Archive for March 10, 2019

ALM Workshop – New York – Feb 2019

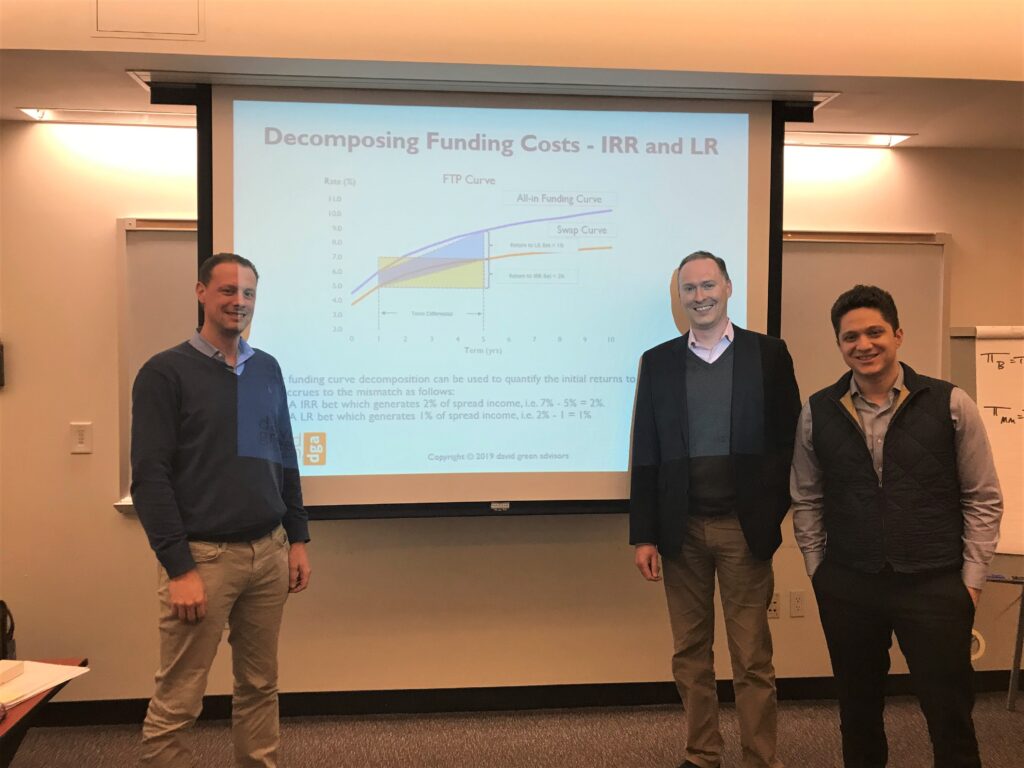

Are you ready for the next move in rates and liquidity spreads? Thanks to Marcus Evans and the delegates to my recent ALM Workshop in New York for another exciting…

Read MoreALM Workshop – Santo Domingo – Feb 2019

Wow, I had an amazing time at my ALM workshop in Santo Domingo (and in Punta Cana afterward!). I want to thank all the delegates (representing all the major banks…

Read More